How to Link Strategic Vision to Core Capabilities

Senior executives commonly ponder such questions as “What might give us continued competitive advantage?” and “What new products should we make or markets should we enter and how?” These questions go to the heart of a firm’s strategic vision — the shared understanding of what the firm should be and how it must change. I present a framework to help managers answer such questions critically and creatively. Knowing the answers constitutes the difference between muddling through and managing with confidence and foresight.

The framework has four steps:

- Generate broad scenarios of possible futures that your firm may encounter.

- Conduct a competitive analysis of the industry and its strategic segments.

- Analyze your company’s and your competition’s core capabilities.

- Develop a strategic vision and identify your strategic options.

The information generated by the first three steps is plotted on a matrix that helps managers see the direction (step four) they should take. The goal is to develop those core capabilities that will be effective for multiple strategic segments in several different possible futures. My approach to strategic vision building belongs to a newly emerging school of strategy called the “resource-based view.”1 Proponents of this approach view the successful firm as a bundle of somewhat unique resources and capabilities. If a firm’s core capabilities are scarce, durable, defensible, or hard to imitate, they can form the basis for sustainable competitive advantage and surplus profit. They also need to be well aligned with the future key success factors of the industry.

The methodology has been applied at corporate and divisional levels in U.S. and overseas firms and to functional strategy development as well (e.g., in marketing and R&D). It can prevent overconfidence and myopic framing of strategic issues from misleading the organization’s planning effort. The methodology has successfully encouraged top management at several companies to break out of traditional frames of mind and challenge conventional wisdom.

Throughout, I apply the methodology to Apple Computer, a company with a case history well known to most managers. I do not intend to explain all of Apple’s strategic problems but to illustrate the complexities of formulating a winning strategy. To establish a foundation for this exercise, I offer the following overview of Apple’s strategic position.

Background: Apple Computer

As the popular story goes, Apple developed in just over ten years from a garage operation into a multibillion-dollar company.2 The Apple II, launched in 1977, was its first real success, and the 1984 Macintosh offered a distinct alternative to IBM in the home and educational segments. However, in the business segment, the Mac had limited software, low compatibility with other machines, and poor networking capabilities. Around 1984, after John Sculley had come to Apple from Pepsico, and founder Steve Jobs was on his way out, the Macintosh Operating Environment concept was launched. The idea was to make Apple machines talk with each other as well as with IBM. However, penetrating the corporate sector proved formidable, given IBM’s deep entrenchment. Concurrently, the desktop publishing capability was developed further, representing an exciting applications area for business as well as home. To assure continued software support, Apple founded a separate software company, Claris, which is focused on Apple computers. Also, it teamed up with Sony, the Japanese electronics giant, to be better prepared for the multimedia era that will integrate television, video, compact disks, and personal computers (PCs). To enhance its foothold in the office market, Apple formed strategic alliances with Digital and IBM, the leading business machine manufacturers.

Meanwhile, the competition had not been quiet. IBM encountered stiff competition from clones, prompting it to launch a new line of PS/2 computers containing a proprietary microchannel. In addition, with the help of Microsoft, IBM developed a new operating system, OS/2, aimed at making Apple’s disk operating system (DOS) obsolete. However, the real gorilla in the PC industry turned out to be Microsoft, since by this time profits and growth were shifting toward software. In the early nineties, Microsoft launched Windows to compete with the look and feel of the Mac, thus boosting its own DOS and undermining IBM’s new OS/2 operating system. In response, IBM teamed up with Apple to attack Microsoft’s dominance in operating systems, although Apple’s real motive seems to be early access to a new powerful IBM chip called Power PC.

The next big technological advance is expected to be “platform independence.” It allows software writers and users to work independently of the operating system being used. Currently, several groups are striving to develop an industry standard. A syndicate led by IBM, Digital, and Hewlett-Packard developed its own version of Unix to compete with AT&T and Sun. The Open Software Foundation developed OSF/l to imitate Unix’s capabilities without being compatible with AT&T products. Increasingly, however, the standards are being set by powerful consumers, not vendors. Numerous customer alliances have been formed, such as the User Alliance for Open Systems, Computer Users of Europe, and the influential X/Open Company, Ltd. In addition, large corporations such as the Hyatt Hotels, K mart, and Aetna are dictating their own standards to vendors. For example, Aetna standardized its 40,000 desktop computers by replacing the 150 or so word-processing systems in use with just one — Microsoft Word.

Other recent developments in the PC industry focus on portable and laptop computers, new input modes such as a stylus (for handwriting), voice recognition, and multimedia integration. Also, virus contamination is increasingly becoming an issue. Over five hundred computer viruses have been documented, and a recent study by the Data Processing Management Association reported that over a quarter of two hundred companies surveyed encountered viruses during January 1991. Today, however, computers can be easily immunized against most viruses. Nonetheless, invidious viruses could cause havoc in the vast community of PCs, unless safe computing practices are adhered to.

Overall, the U.S. market for personal computers amounted to $45 billion in 1990 sales. This domestic market was divided among the major manufacturers as follows: 16 percent share for IBM; 11 percent for Apple; 7 percent for Zenith and Compaq each; and 3 percent for Tandy.

Scenario Analysis

In such an uncertain industry with such intense competition, a company needs a method of analyzing its environment that is more fundamental than the typical methods of scanning and trend analysis.3 Companies confronted with major uncertainties, life-threatening competition, or sudden discontinuities may find the scenario method usefu1.4 The scenario method helps managers map out a wide range of possible futures, forcing them to “think outside the box.”5 The method is well suited for addressing such external changes as deregulation, foreign competition, new technology, and increased environmental concerns. It exposes managers’ assumptions (e.g., the government is the enemy) and knowledge gaps. Too often, corporate views about the future are myopic, short-term, or concerned only with a few data points.6 Scenarios can challenge conventional wisdom and stretch people’s thinking so they better appreciate long-term threats and opportunities.

The basic idea in scenario construction is to identify existing trends and key uncertainties and combine them into a few future worlds that are internally consistent and within the realm of the possible. The purpose of these scenarios is not to cover all eventualities but to discover the boundaries of future outcomes.

Time Frame and Scope

The first step is to determine the appropriate time frame and scope of the analysis. Imagine that we are managers at Apple, charged with conducting this exercise. We list several factors that might affect our choice of time frame: technology changes, product life changes, competitor time frames, and the firm’s “investment intensity” (see Table 1). We decide that a five-year time frame is appropriate. Although long by product innovation standards (Apple once changed its entire product line in about 100 days), five years is medium-term relative to operating system generations. Operating system life cycles have been on the order of ten years. In other industries, the time frame would depend on other factors. For example, a company such as Chrysler has pursued investment levels over the past decade that enabled it to rebuild itself in about five years. For other firms, such complete corporate renewal might take ten years, in which case a longer time horizon would be appropriate.

{kind=link}

Next, we need to determine the scope and stakeholders (they can always be revised later if necessary). For Apple, we need to choose product scope, technology scope, and geographic scope. Let’s say that for this analysis we choose personal and minicomputers, both software and hardware, in an international arena.

Regarding stakeholders, all parties affected by personal computing should be considered, especially if they can flex their muscles. Over time, software producers have become increasingly important, as have clone manufacturers. And powerful customers exert more and more influence on standards the industry might adopt for operating systems and software for user interface.

Trends and Uncertainties

The second step is to identify existing trends and conditions that will significantly affect the industry’s future in known ways. Influence diagrams and causal maps are useful tools to revel perceptions about trends and their interrelationships.7 The trends must be mutually compatible within the given time frame and widely agreed on.

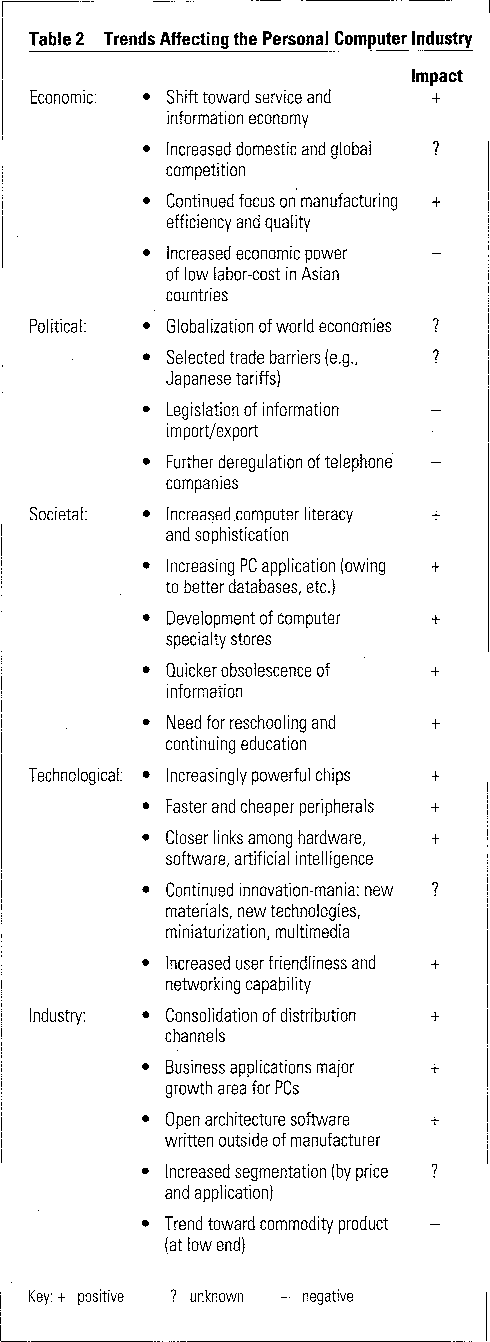

Table 2 lists the strategically important trends we might identify for Apple. These twenty-three trends cover the economy, politics, society, technology, and the industry. They range from the shift toward a service and information economy to the trend toward computers becoming low-end commodity products. These are trends that Apple managers are likely to agree on.

{kind=link}

Those trends that are not consensual should be treated as uncertainties, the third step in scenario construction. To identify key uncertainties, which is the heart of scenario thinking, it is useful to ask what three or four fundamental questions managers would like to pose to an oracle of Delphi, such as, “Will there be a fundamental technological breakthrough?” and “Will the United States-Japan trade conflict intensify or subside?” Other approaches to identifying key uncertainties are to examine issues of policy dispute or important upcoming decisions.

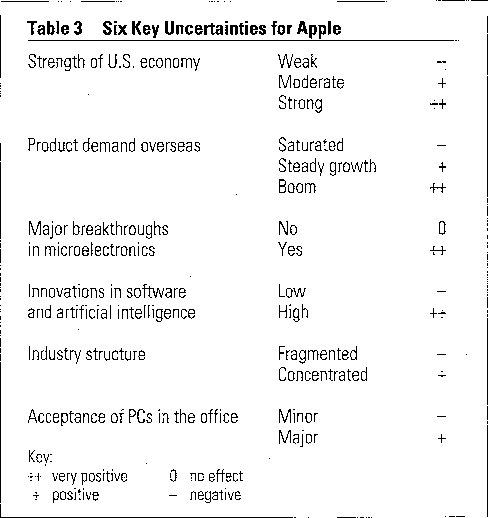

Table 3 lists six key uncertainties for Apple, with various possible outcomes and an assessment of their impact on the company. For example, we can’t know yet what product demand will be like overseas, but we know it is an important concern. If overseas markets become saturated, Apple will be negatively affected. Steady growth would be positive for Apple, and a boom would be very positive. Here, these outcomes and assessments are simplified and represent my views. In practice, the management team would generate these alternatives and would back them up by any objective analyses available or feasible. Many judgments, however, would remain subjective.

{kind=link}

At this point, it is useful to discuss any interrelationships among the key uncertainties. For instance, a strong U.S. economy is likely to increase PC sales, spur research and development (R&D), and attract competitors. The latter, in turn, decreases industry concentration. Formal m6dels can be used to capture such interconnections using cross-impact analysis or other conditional probabilities.8

In step four, the trends and uncertainties are combined into internally consistent, coherent, and wide-ranging scenarios. Do not limit yourself to internal viewpoints; vigorously pursue contrarian beliefs and outside perspectives.

To develop the scenarios, it is useful to start by putting all the negative elements in one scenario and all the positive elements in another. Thus, the “all bad” scenario for Apple would be:

Asian countries continue to undercut U.S. products and flood the market with low-cost clones. Governments forbid free transfer of data across national boundaries, adding costs and delays to international data transfer. Telephone companies enter the PC business more vigorously, first via peripherals (e.g., voice and interfaces) and then by marketing and building the machines themselves’. The commodity nature of low-priced PCs erodes profit margins. The U.S. economy is on the brink of recession, demand drops, and organizations are slow to embrace distributed computing.

An important question is whether this scenario (as well as any other) is internally consistent. For instance, are low product demand and a fragmented industry structure compatible outcomes in the above scenario? And should greater deregulation of telephone companies and more computer specialty stores perhaps be in the same scenario?

Similar questions of consistency exist for an “all good” scenario. It is often a matter of judgment whether certain elements go together. No simple recipe exists for creating consistent scenarios, nor would this be desirable. These extreme scenarios just offer wide starting points from which to develop different but consistent scenarios. Using common sense and strategic reflection, we might develop the following three scenarios as useful backdrops for Apple’s strategic thinking.

Scenario 1: Stagnation and Saturation

Personal computer sales slow down to a point of near stagnation owing to a severe economic recession in the United States. Domestic firms attempt to defend and preserve market share through drastic price reductions resulting in major erosion of profit margins. The industry, led by IBM, creates a weak standard to enhance networking capabilities. This standardization turns the PC market more into a “commodity habitat” with highly elastic demand. IBM is moderately successful in integrating the PC with other products (such as telephones and measurement and control devices) even though it seeks to dominate these new markets through synergistic relationships with its subsidiaries. The real winner in this stagnant and stalemated world is Microsoft, which controls the operating system for IBM and its clones while offering interface capabilities that are similar to those on the Mac.

The office market proves to be the largest and most profitable PC segment. Other segments, especially school and home, “fizzle out” because of budget crises and uncertainties about standards and obsolescence of new products. Increasing concerns about computer viruses scare off less sophisticated users. The data processing and purchasing departments of large corporations work hard to develop plans that integrate personal computers into corporate EDP programs. Networking becomes the key strategic objective of EDP departments, which often adopt their own standards. IBM PCs are widely viewed as the product most likely to be integrated with other capabilities already in place. Apple, despite its innovative product line and user friendliness, is not seen as integrating well with existing and future IBM systems.

Scenario 2: Computer Confusion

Moderate growth in the U.S. economy is causing modest growth in the computing and PC markets worldwide. Expecting a boom, numerous companies had entered the PC business, including several large technology companies. However, consumers are increasingly confused about competing claims made by vendors, and the lack of an industry standard keeps many buyers on the fence. The shifting alliances among IBM, Apple, and Microsoft make it difficult to predict what systems will prevail. In addition, computer virus epidemics flare up occasionally; reminding consumers of their vulnerable dependence on PCs. Overall, the PC and peripheral industries exhibit fierce competition for hesitant and rather confused consumers.

The large range of choices available discourages large users from committing to any particular manufacturer or technology. Customers’ decisions are influenced by a variety of factors including price, support, software features, expandability; manufacturing quality; distribution, image, and marketing. New technologies and concepts catch on slowly, and user needs remain ill defined. Foreign markets are likewise developing slowly, although no unusual trade barriers have formed.

The business segment continues to demand increased networking capabilities. However, no industry networking standards seem to be emerging in the near future, resulting in piecemeal approaches to networking efficiency. Throughout this period, IM continues to dominate the business market for all sizes of computers (PCs, minicomputers, and mainframes), without any dramatic changes in its PC strategy.

Scenario 3: Computer Cornucopia

The U.S. economy is booming. The U.S. dollar is weak, thus increasing export opportunities, including to Eastern Europe. Both the U.S. and global PC markets are growing, especially in the education, small business, and government sectors. In addition, the market for peripherals and software is expanding quickly. PCs are being built into new upscale homes (as microwave ovens and intercom speakers are today) to manage the heating, electricity, water, and electronic systems (such as security alarms, speakers, and televisions). Laptops and portables are commonplace, and they have electronic pens for handwritten input.

The information age revolution, coupled with favorable economic conditions, instills increased consumer sophistication regarding the use of personal computers. The industry develops practical networking capabilities, platform independence, and increased computer power at the PC level, thereby virtually eliminating minicomputers. PCs are able to interact with a variety of machines and products in most user environments. Major new developments occur in software technology based on artificial intelligence (especially voice synthesis and language comprehension). The application expansion fuels the demand for PC education and literacy in schools. The PC market, responding to consumer demand, experiences accelerated, rapid growth.

Competitive Analysis

Whereas scenario analysis explores the general environment; competitive analysis focuses on each company’s unique position, taking into account industry structure and the firm’s own evolution. The industry analysis focuses on the forces and barriers (both entry and exit) to competition; the existing economies of scale, scope, and experience; and the stage of industry development, from emerging to mature and declining.9 It also includes softer analyses such as the attitudes, reputations, and past interactions among the players in terms of retaliation, coalitions, commitments, and so on. The nature of the industry partly determines the competing firms’ size distribution (e.g., fragmented versus oligopolistic), scope (e.g., single versus multiproduct or domestic versus global), and strategies (low cost versus differentiation or innovation versus imitation).10 Also pertinent are the competing firms’ unique histories and evolutions, as these determine what kind of resources and capabilities they have at their disposal.

The PC industry has been in great flux owing to technological innovations and globalization. Overall, it is an emerging, fragmented, highly competitive industry in which the largest player, IBM, has about 16 percent market share. Entry barriers consist of know-how, capital, reputation, and distribution networks. Nonetheless numerous clones and unauthorized manufacturers have entered, highlighting the difficulty of protecting any proprietary design short of using a closed architecture. The industry has expanded very quickly — to nearly $100 billion worldwide in 1991 — and it is unclear whether or when PC saturation will occur in the United States, Europe, or other key markets. New technologies can make earlier models obsolete within a year or even months (as in the case of laptops and notebook computers), making product cannibalization an important strategic issue. Network externalities are also key since PCs are increasingly used as a communications good. Just as telephones and fax machines increase in utility as more people have them, so do PCs and software. Although first-mover advantages might be expected in this rapidly changing industry, IBM was a late entrant and still became the most dominant PC manufacturer. The industry uses a variety of distribution channels, such as direct sales (to educational buyers), retail stores, and system integraters (for small and large business).

Apple’s own competitive position is one of maverick and trendsetter. Apple grew quickly because it was first with a hit product, the Apple II. Its success, however, soon attracted other players. Moreover, Apple squandered its precious lead on the competition through internal turmoil and misreading of the market. For example, the schism between Steve Jobs and John Sculley caused divisiveness and the departure of key people. During the late 1980s, Apple priced its Mac too high while stocking up on very expensive memory chips that later dropped greatly in price. Also, Apple was late in exploiting the trend toward portables and notebooks, in part because its first portable was not well liked. Nonetheless, Apple enjoys a unique image — of fun, innovation, user friendliness, and brashness that may serve it well in certain segments of the market, such as home and education. However, this same image may be a hindrance in the stodgy world of business. Apple’s traditional desire to be independent will hurt it in developing important strategic alliances, especially if the industry moves more toward consumer electronics and fuller media integration. Apple’s recent alliances with Sony (for its laptop) and IBM (for new product development), however, signal a change in strategy. To fully understand Apple’s competitive position, we must carefully examine each strategic segment in which it currently competes or might compete in the future.

Strategic Segmentation

The next step after competitive analysis is to identify all significant strategic segments the firm is or might be competing in. This is important because recent research suggests that, on average, profitability varies far more across businesses within an industry than across industries.11 The focus of analysis, therefore, should be on each strategic business unit of the firm, within its industry context.

The concept of business segmentation has a long history, starting with product segmentation in the 1950s, market segmentation in the 1960s, and product/market segments in the 1970s and 1980s.12 In product segmentation, the focus is on the varying requirements and strategies from a manufacturing viewpoint. In market segmentation, the relevant aspects are the different needs and characteristics of each customer group. In strategic segmentation, the aim is to highlight and delineate the important but essentially different battlefields the firm is or might be competing in. Consequently, the focus is on such strategic factors as technologies used, customer needs satisfied, marketing channels, growth rates, innovation, forces of competition, entry and exit barriers, pricing practices, distribution channels, value chains, customer profiles, government regulation and protection, and so on.13

The business segmentation task can be approached top down, a practice followed by the consulting firm Strategic Planning Associates, or bottom up, as favored by the Strategic Planning Institute. It can be performed intuitively or systematically.14 In the latter case, multidimensional scaling and cluster analyses may be useful tools to distill the relevant bases of segmentation and to identify the major segments.15 Whatever procedure is used, the analysis should yield a limited number — from two to eight — of business segments that differ fundamentally in their strategic nature. These strategic segments need not be pure, such as only product groupings or customer segments, but can be hybrids of product, market, technology, distribution, region, and pricing features.

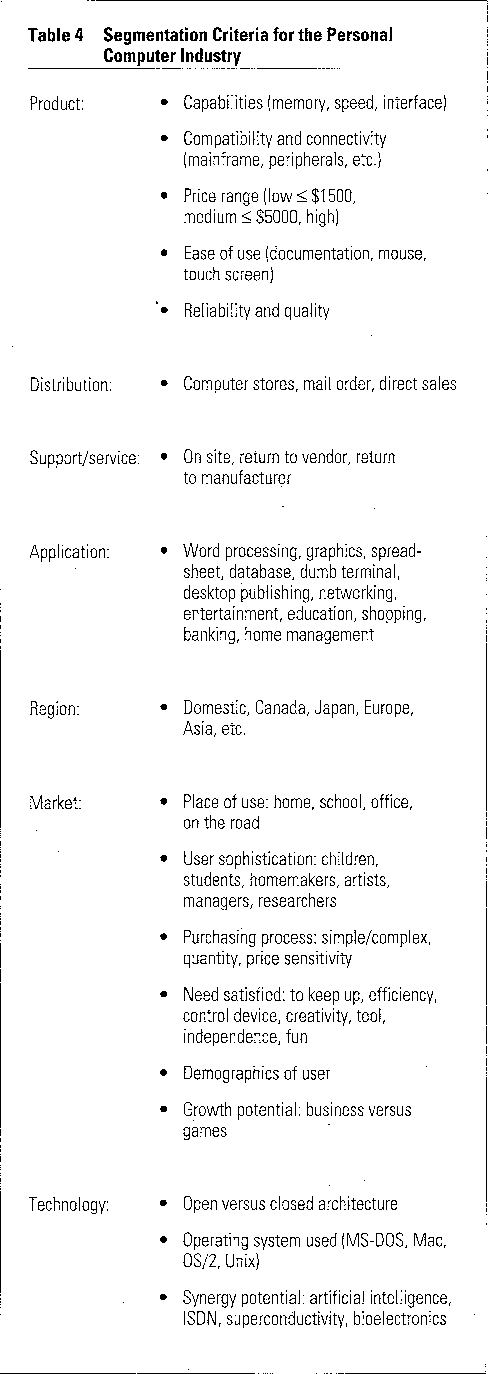

A large number of criteria can be used to segment the PC industry, from geographic to product lines to types of applications and users (see Table 4). For example, one segment would be home use of low-end computers for video games in the northwest United States. At this level of detail, ‘there are hundreds of separate segments in which Apple competes. However, such detail is counterproductive for strategy development since not all these segments are strategically different. In deciding whether two segments are strategically different, we should examine:

{kind=link}

- each segment’s market size, both present and future;

- customer and product differences;

- the kind of competitors and strategies encountered;

- the distribution channels used; and

- differences in suppliers, regulators, unions, and so on.

Unless two segments are different in at least two of the above criteria, they are probably not truly distinct strategic segments, although they might be very different from just a marketing or manufacturing perspective. Based on this kind of analysis, we might identify the following six strategic segments for Apple:

Big Business.

Large quantities purchased; central purchasing; limited price sensitivity; less need for user friendliness; high need for networking capabilities; computing power important.

Small Business.

Smaller quantities purchased; individual buying decision; more price sensitive; more need for user friendliness; low need for networking capabilities.

Home.

One unit purchased; individual buying decision; very price sensitive; high need for user friendliness; low need for networking capabilities.

Education, University.

Large quantities purchased; central purchasing; more price sensitive; less need for user friendliness; high need for networking capabilities; computing power and sophisticated software important.

Education, Elementary.

Large quantities purchased; central purchasing; more price sensitive; high need for user friendliness; high need for networking capabilities.

Workstations.

Small quantities purchased; individual or group buying decision; less price sensitive; less need for user friendliness; high need for networking capabilities (via servers, etc.); computing power and speed very important.

The purpose of strategic segmentation is to understand in detail which competitive forces and barriers are significant within each segment.16 For each battlefield, we should examine how powerful the following forces of competition are and what barriers protect the firm from each:

- rival firms offering similar products and services;

- suppliers of components, labor, capital, and managerial talent;

- customers who desire lower prices and better service;

- potential new entrants; and

- government (i.e., taxes and regulations).

For instance, being well diversified in suppliers is a key barrier against profit erosion by vendors. For Apple, high switching cost (in going from IBM to Apple or vice versa) is another important barrier against consumers competing away profit by shopping for the lowest price.

Also, we must know who the rival firms are in each arena or battle. For instance, in the business segment, Apple encounters IBM, Wang, Hewlett-Packard, Zenith, Compaq, and so on. In the workstation market, it is up against Sun Microsystems, Digital, Next, and Hewlett-Packard. In the educational and home markets, key competitors include Commodore, Atari, and Tandy’s Radio Shack. In addition, Apple faces various new entrants in the nonbusiness segments such as IBM, AT&T, and Asian manufacturers, including NEC, Toshiba, and Hyundai. On the supply side, Texas Instruments, Motorola, and Asian chip producers could seriously erode profits. Finally, in foreign markets, governments could be a formidable force of competition through trade restrictions and taxes. Significant barriers in these various segments include switching costs, reputation, installed base, customer access, and patents.

The overall objective of competitive analysis is to decompose the industry into its strategic segments and study the competitive structure within each segment in terms of barriers and competitors. For purposes of further analysis, we shall reduce Apple’s strategic segment from six to four, namely home, education, business, and workstations. These distinct segments constitute four important strategic business units (SBUs) for Apple.

Core Capabilities

Thus far our analysis has been externally focused — on the general future environment and competitors. The next step is to examine the firm internally, in terms of its core capabilities. The traditional approach is to score the firm on a large number of attributes, such as relative strength or weakness in R&D, engineering, manufacturing, marketing, sales, product quality, product line, employee morale, compensation, quality of personnel, reputation, .and so on. Not all of these attributes, however, are of equal importance strategically. Moreover, many are symptoms of more fundamental characteristics that define the firm’s essence. There are several ways to ascertain these more basic features.

The Firm as an Onion

Think of the firm as an onion made up of layers of functions, services, and production operations. Then ask which activities determine the firm’s essence or core and which are at the periphery. For example, the outer layer may include product design, selling, or even marketing for one firm, whereas these skills and capabilities might constitute the core of another firm. Honda’s core consists of the design and manufacturing of engines, which underlie its strengths in passenger cars, motorcycles, lawn mowers, and race cars. Other car manufacturers have different cores. Chrysler, for example, subcontracts major portions of its engine design and manufacturing. For biotech firms, a core capability would be R&D, including how to access academic know-how and commercialize it through strategic alliances. Selling and marketing, in contrast, fall in the outer layer for those biotech firms that license their products to established pharmaceutical firms.

The Firm as a Tree

An alternative way to explore core capabilities is to think of the firm as a tree.17 In this metaphor, the leaves and fruit represent the firm’s end products and services. The branches constitute SBUs, which combine related products or services (e.g., midsize cars, heavy-duty lawn mowers, and 500cc motorcycles). The trunk denotes core products, such as engines in Honda’s case, which support each of the SBUs and end products. Lastly, the roots represent capabilities or core competencies that enable the firm to sustain its existing branches and grow new ones. Unlike a core product, a core capability (or competence) is not a stand-alone, sellable service or commodity. Examples of potential core capabilities include high-quality manufacturing, good supplier relations, service excellence, innovation, short product development cycles, well-motivated employees, a marketing culture, and a strong service reputation. The challenge is to think of the firm not just in terms of its visible end products but also in terms of its invisible assets and core capabilities.18

Strategic Assets

Above-average return can derive only from assets and skills that are hard to imitate. By definition, these assets and skills cannot be bought off the shelf but must be developed over time through investment and information exchange by the firm’s human capital.19 By their nature, they involve time and evolution. For example, Apple could not have produced the Macintosh without learning first from the success of its Apple II and then from the failures of its Apple III and Lisa computers. This learning path entails micro-level interactions (among people, groups, and functions) that are hard to script, imitate, or even document. Indeed, the idiosyncracy of this learning process is a desirable and necessary condition for competitive advantage. It makes a firm more immune to competition. For instance; 3M’s well-known culture for innovation and Wal-Mart’s distinctive approach to multiservice stores evolved in ways that are hard to duplicate and even harder to imitate swiftly.

In sum, firms differ fundamentally in the resources and capabilities they control. And since their capabilities developed slowly, firms are usually stuck with them in the short run. These “sticky assets” reflect the firm’s unique history and limit the range of strategies realistically available to a firm. IBM could never become an Apple, nor Apple an IBM. Both have unique experiences and capabilities. It is crucial to understand what a firm’s present core capabilities are and to what extent they need to be adjusted or replaced in view of the future scenarios. The following characteristics help define a core capability and can be used to score it relative to other core competencies:20

- It evolved slowly through collective learning and information sharing.

- Its development cannot be greatly speeded up by doubling investments.

- It cannot be easily imitated by or transferred (sold) to other firms.

- It confers competitive advantage in the eyes of customers.

- It complements other capabilities in a 2 + 2 = 5 fashion.

- Investment in it is largely irreversible; that is, the firm cannot cash it out.

Key Success Factors

The identification of the core capabilities must occur in the context of an industry’s key success factors (KSF).21 Think of KSFs as those strategic variables that a historian will pick to best discriminate winners from losers in your industry. For example, looking backward, raw material sourcing proved to be a KSF in the uranium and petroleum industries. Economies of scale were critical in steel and shipbuilding. Quality design was a core capability in the aircraft and stereo industries. For beer, films, and home appliances, distribution has been of overriding importance.22 The challenge in articulating a strategic vision is to identify the most important industry KSF, then to determine which core capabilities should be developed for one’s own firm.

Apple’s Core Capabilities

Apple’s unique role as the creator of the PC industry endowed it with distinct resources and capabilities. Foremost is that of innovation. Apple has been highly creative in product design, manufacturing, and the use of advertising. In product design, the mouse and icons were just the start. The look and feel of the Macintosh is only now being imitated by Microsoft’s Windows. The do-it-yourself: simple startup of Apple’s products helped it greatly in the personal and home markets. And in the mid-1980s, it used award-winning television commercials to entice average consumers to take a “test drive” with the new Mac. It also streamlined its organization during this time period, under Sculley, bringing coherence to its product line and greater efficiency to its manufacturing.

Some of these capabilities have somewhat eroded, however. Frequent reorganizations signaled dissatisfaction with the overall strategy and implementation. The business segment proved much harder than expected, in spite of a national salesforce and heavy promotion. Nonetheless, the following capabilities capture much of Apple’s essence during the 1980s:

- Reputation for user-friendly, innovative products;

- Culture of risk taking, defiance, and entrepreneurship;

- Pursuance of bold, billion-dollar visions;

- State-of-the-art technology and design;

- Educational franchise developed over many years;

- Loyal customer base, especially in homes and schools;

- Excellent brand awareness in all key markets; and

- Creative and effective use of print and television advertising.

Also, Apple is the only PC manufacturer of systems software, central processing units, and peripheral equipment, such as printers. Unfortunately, the above bundle of capabilities may not be enough to see Apple through the 1990s. Clones, new players, different technologies (e.g., multimedia), a reborn IBM, new markets (in Eastern Europe), and so forth may require new and stronger capabilities. The above list is a platform from which Apple must operate — it both confines Apple and gives it a competitive edge. The challenge is to formulate and implement a vision that builds on existing strengths and mitigates the company’s weaknesses, such as its past insistence to go it alone. Also, the vision should identify new core capabilities to be developed or coopted, such as electronic miniaturization, broad-based technical support for large organizations, and rapid access to Eastern Europe.

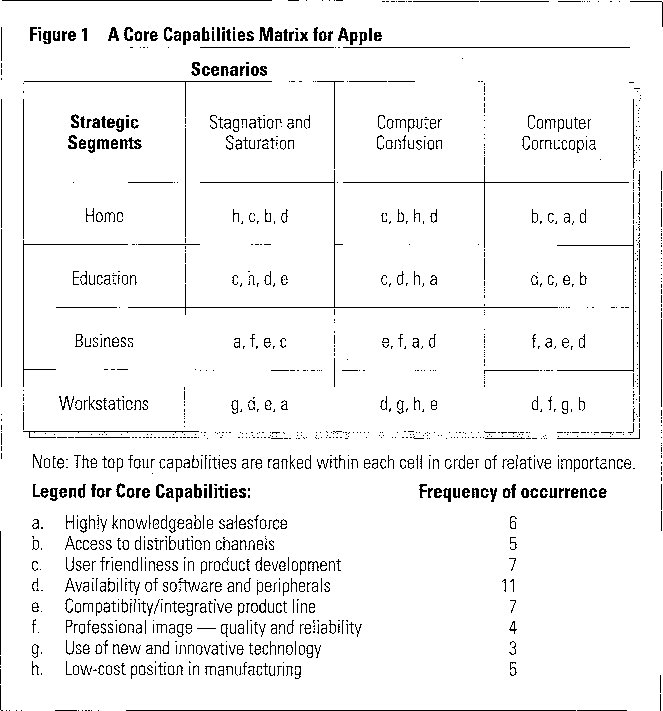

Core Capabilities Matrix

A strategic vision pulls together the insights obtained from examining the multiple scenarios, the industry’s competitive structure, and the firm’s (and competitors’) distinct core capabilities. It helps to focus managerial attention and indicate which core capabilities the firm must develop further and how, so as to succeed in its chosen business segments.

Deciding which core capabilities should become the drivers for the future can be done systematically by juxtaposing the scenarios and the strategic segments. Figure 1 shows how a core capabilities matrix can be used to do this. This matrix, using Apple’s core capabilities, lists the strategic segments on the vertical axis and the scenarios on the horizontal axis. For each cell, the core capabilities are listed that would help the firm do well in that segment under that scenario. Remember to use only those capabilities that are unique, important, controllable, durable, and that can generate excess profit.

{kind=link}

One of the most important ways to look at the matrix is to identify the core capabilities that will be effective for multiple segments in a variety of future worlds. These are the capabilities a firm will want to leverage. They should be clearly identified and made an integral part of the company’s overall strategic vision.

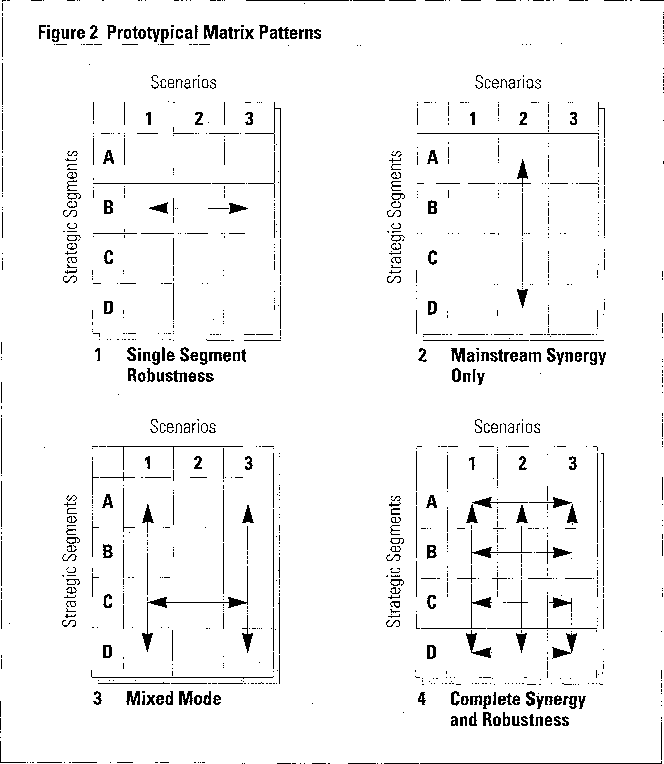

Let’s look at some possible matrices. Figure 2 shows some prototypical matrix patterns. In matrix 1, a company operates in four strategic segments and has envisaged three possible future scenarios. The only place where core capabilities overlap is in segment B. An example might be a pharmaceutical firm’s ability to get Federal Drug Administration approval (the core capability), which may be crucial for its patented drugs (segment B) in all possible futures. In other segments, each scenario requires a different set of core capabilities. Naturally, one’s odds of success are greater if capabilities are developed that add value for multiple segments.

{kind=link}

Matrix 2 depicts a company that will reap above-average returns, given its core capabilities, only if one scenario comes to pass. For example, superior brand management or service reputation could pay off in several product markets. This firm has a competitive advantage over firms operating in only one of these segments, but if one of the other scenarios comes true, if one of the other scenarios true, its advantage may not mean much.

The more unique the capabilities and the more they overlap, the greater and more complex are their synergies. In matrix 3, there will always be some kind of synergy for segment C, no matter the future scenario, and this firm has greater odds of being competitive in the other segments, as they look strong for two of the three scenarios.

The ideal case would be matrix 4, with overlapping core competencies in every segment for every scenario. However, there is no guarantee that this state is achievable. A company may be able to achieve it by developing only those capabilities that are required in all cells, but if other important capabilities are thereby neglected, this approach will have its downside, too.

Of course, it may be that few core capabilities appear more than once per cell. In that case, there may be no basis for a strategic vision in which multiple capabilities function in harmony at the corporate level. The firm may be little more than a collection of distinctly different companies operating in strategically different segments, whose core capabilities do not reinforce each other. Such lack of synergy is a serious issue. It could cause conflicting signals and confusion, as multiple driving forces need to be managed and coordinated. Thus, strategic visions need to consider issues of organizational design, skill sharing, and culture. They must also address what practical options exist for moving the company in the desired direction.

It is instructive to rank the core capabilities within each cell because this naturally leads you to examine why rank-reversals occur across scenarios or segments. Also, it helps identify the robust and synergistic core competencies around which marketing, production, R&D, and personnel plans should develop.

No simple formula exists for identifying and ranking the core capabilities in each cell. This requires seasoned managerial judgment, creativity, and a keen sense of each segment’s competitive structure.23 Scoring the various capabilities on the characteristics listed under “Strategic Assets” above will be helpful.

Apple’s Vision and Options

Without the benefit of the matrix analysis, several strategic visions appear to make sense for Apple a priori, such as:

- Remaining a leading-edge hardware manufacturer;

- Creating integrated hardware-software products;

- Attacking IBM head on in the business market; and

- Becoming a consumer electronics company.

The matrix analysis suggests that the second and fourth visions listed above make the most sense for Apple. Wide availability of software and peripherals for Apple’s computers is the most frequently occurring key success factor in the matrix, followed by high compatibility with competing products and high user friendliness. Considering these future KSFs and Apple’s current resources and capabilities, the vision of creating integrated hardware-software products and reorienting the company toward consumer electronics in general has much to recommend it. Hence, based on the matrix of Figure 1 and Apple’s unique capabilities profile, I favor this vision:

To be a company that offers innovative but affordable computers for individuals. It will provide the most user-friendly operating system and software available. Apple will continue to be a major player in the business segment, emphasizing people rather than machines. However, the overall strategy is to become a consumer-oriented electronics company focused on communication and information processing products.

While this vision may seem quite general, it is significantly different from the visions of Apple’s major competitors and ties directly to Apple’s core capabilities. Contrast these three visions:

- Apple focuses on innovative electronic consumer products using computers.

- IBM emphasizes distribution and service for business using networked computers.

- Clones stress quick imitation, high quality, and low prices (but not innovation).

Note how IBM’s vision of PCs is fundamentally different from Apple’s. For IBM, the I PC is primarily a linkage mechanism to mainframes. For Apple, PCs are I truly personal devices that can connect with a host of others, but are sold as stand-alone electronic products.

Strategic Vision

Although firms seldom publish their visions in detail, several examples have been described in the business press. Dow Chemical pursued a vision and framework developed by Herbert Dow over fifty years ago.24 It called for innovative manufacturing, forbidding copying or licensing; gaining control of raw material supplies; pursuing economies of scale and scope via vertical integration; and continually expanding capacity over business cycles. Essentially Dow’s vision was to become a large-volume producer of commodity chemicals. This vision served it well for many decades, although Dow has lately focused more on specialty chemicals and higher-margin products.

Another venerable and successful vision guided Crown Cork & Seal. Until 1977 it pursued a strategy of being a differentiated low-cost producer of steel cans, crown bottle tops, and related container machinery for the beer, soft drink, food, and aerosol markets. Its competitive advantages derived from a low-cost position, flexibility in delivery, strong technical service, and a full line of packaging material and equipment. Crown’s vision, however, also required major adjustment when some of its major markets were threatened, for example, by aluminum can makers. Thus, visions do not last forever and need periodic reassessment. For several decades, clear visions provided guidance and focus for these two organizations while generating high returns.

A sound vision that has been articulated and communicated by top management raises the firm’s “strategic I.Q.”25 Lower-level echelons first internalize the vision and then pursue products and markets in line with it. Hence, a strategic vision helps managers decide which products and markets should and should not get resources. Even though a particular business may be profitable, unless it reinforces the core capabilities called for in the vision, it should not be high on the list for funding. In this sense, having a strategic vision redefines the rules for acting opportunistically or incrementally. The vision determines strategies, plans, and budgets. Similarly, the incentive system and performance reviews should be operationally linked to the vision and the strategies it calls for. This is the challenge of true strategic management.

Why should this method for generating a sound vision work? Strategic plans are essentially investments under uncertainty. Developing those core capabilities that will be effective in different futures positions the firm to do well in any future. And if those core capabilities are not easily imitated or destroyed, then when competitors realize the importance of those capabilities, they will not be able to easily acquire them.

Further, if the core capabilities overlap in multiple segments, the firm has more opportunities for success. A firm competing in four segments has six opportunities for synergies within pairs of segments, three possibilities for three-way synergies, and one chance at a four-way synergy. Juxtaposing these synergy opportunities with those of competitors should reveal if and where sustainable competitive advantages might be garnered.

The purpose of the matrix analysis, however, is not to instill risk-aversion or excessive hedging. It is primarily an aid in deciding which capabilities to emphasize in view of their synergies over segments and resilience under different scenarios. This is done by first examining each cell in isolation and thereafter comparing the required capabilities across cells. Once the degrees of synergy and robustness have been ascertained, it can then be decided whether to play it safe (by developing primarily the common capabilities) or go all out and bet the company on one particular scenario or segment. As an empirical conjecture, I expect that firms that earn persistently high returns do so to a large extent by capitalizing on overlaps in their core capabilities matrix. Whether column or row overlap is more valuable will depend on time frames, risk levels, growth prospects, competitors, and other factors that are beyond my scope.

Implementation

Once a firm has chosen one vision from among those that make sense, it must rethink its organizational design, culture, driving forces, and incentives. Ideally, a new vision builds on what already exists rather than requiring demolition. Again, I use Apple to illustrate.

Organizational Fit

The strategic vision described above accords well with Apple’s current strengths, although it differs starkly from what the company used to be. In the past, Apple was a highly informal, unstructured company; in which technological breakthroughs were mainly accomplished by isolated product champions. Products were often developed independently from previous ones, and integration of products was minimal, owing to internal competition. The user friendliness of Apple’s operating software, in contrast, has been one of its major strengths and should remain a distinguishing feature.

Structural Changes

The vision requires continued emphasis on software development, in the form of either a new division or a new company. This software unit should work closely with the hardware development group, and ideas should be generated bottom-up. Thus, the organizational structure should be as horizontal as possible to encourage informal interaction. It’s important that the marketing group establish closer links with the new product group as well as the software group.

Driving Forces

Technology and the closely related issue of user friendliness should remain the primary driving forces of Apple’s vision. The technology emphasis will come through the R&D department, which, together with the marketing group, should remain focused on the needs of its customer base, especially in the business segment. This may require special incentives that encourage intrafirm collaboration and teamwork. In general, Apple should seek to remain at the leading edge in transforming the industry from hardware-driven to emphasizing software and end users, while focusing on home entertainment, desktop systems, and communication devices.

Strategic Options

Strategic options are the vehicles through which a sound vision gets implemented and realized. Their creative generation and subsequent evaluation merit special attention.26 Early on, it may be detrimental to evaluate strategic ideas in narrow financial terms, as it will be difficult to price out properly all synergies and strategic benefits.27 Each strategic alternative has an option’s value that must be properly assessed.28

Apple’s vision requires a strong focus on technology, integration, and software. The following are some specific strategic options to illustrate how Apple can start to realize its vision:

- Open Architecture. Although an open architecture invites imitation, it also encourages compatibility of peripherals, software, and components, which is especially important for the business market.

- Software Joint Venture. Apple has already embarked on this route, recognizing that it takes more than hardware to sell PCs. However, hardware and software development may have to be integrated more closely yet.

- IBM Compatibility. Although AppleTalk enables users to network with other systems, how far should compatibility be pushed? If the vision calls for conquering the business segment, compatibility is critical.

- Product Line. Should Apple specialize in only certain PC types or offer a complete line? Again, in the business market a full line that is compatible and upgradable may be necessary.

Conclusion

This paper has examined how management teams might develop and test strategic visions to enhance future survival. Resilience is the key to prospering in a variety of futures, so it should be an important test of strategic vision and direction. Resilience or robustness does not just encourage optimization within the expected scenario but offers increased survival chances under less probable but potentially devastating scenarios.

A Team Effort

Since multiple perspectives are needed, explicit vision building or testing is best conducted in small groups. In my experience, management teams need no more than two or three days to apply the above process at a, qualitative, broadbrush level to their own situation. Especially if managers have done prior work on competitive analysis and understand past key success factors, the process can happen quickly once sound scenarios have been developed. Flexible facilitation, including techniques that encourage creative, nonlinear thinking, is essential to the successful application of this process in management teams. Usually, follow-up staff work is indicated for the scenarios or competitive portions, and external consultants may be useful if limited in-house resources or expertise exist.

This overall approach emphasizes a resource-based view of the firm. It is aimed at identifying and evolving those core capabilities that are important in multiple segments under alternate scenarios. By focusing the strategic vision on core capabilities needed in various possible futures and multiple strategic segments, synergies can be developed that give rise to surplus returns. Of course, these capabilities must not be easily transferable, for example, by a competitor merely hiring away a key employee. The less imitable the core capabilities are, and the more they indeed turn out to be the discriminating factors for business success, the greater their economic return. A firm’s strategic vision essentially boils down to a bet on some perceived future or futures. The present methodology hedges this bet against a broad range of scenarios, while extracting as much as possible from existing synergies. It strives for synergistic resilience in the development of a firm’s core capabilities.

References

1. See D.J. Teece, “Toward an Economic Theory of the Multiproduct Firm,” Journal of Economic Behavior and Organization 3 (1981): 39–63;

B. Wernerfelt, “A Resource-Based View of the Firm,” Strategic Management Journal 5 (1984): 171–180;

J.B. Barney, “Firm Resources and Sustained Competitive Advantage,” Journal of Management 17 (1) (1991): 99–120; and

R. Amit and P.J.H. Schoemaker, “Strategic Assets and Organizational Rent,” Strategic Management Journal (in press).

2. For details, see C.C. Swanger and M.A. Maidique, “Apple Computer: The First Ten Years” in Strategic Management of Technology and Innovation, eds. R.A. Burgelman and M.A. Maidique (Homewood, Illinois: Irwin, 1988), pp. 288–320.

3. E.P. Learned, C.R. Christensen, K.R. Andrews, and W. Guth, Business Policy (Homewood, Illinois: Irwin, 1969); and

K.R. Andrews, The Concept of Corporate Strategy (New York: Dow Jones-Irwin, 1971).

4. S.P. Schnaars, Megamistakes: Forecasting and the Myth of Rapid Technological Change (New York: Free Press, 1989).

5. See P. Wack, “Scenarios: Uncharted Waters Ahead,” Harvard Business Review, September–October 1985, pp. 72–89;

W.R. Huss, “A Move toward Scenarios,” International Journal of Forecasting 4 (1988): 377–388; and

P.J.H. Schoemaker, “When and How to Use Scenario Planning: A Heuristic Approach with Illustration,” Journal of Forecasting 10 (1991): 549–564.

6. J.E. Russo and P.J.H. Schoemaker, Decision Traps (New York: Simon & Schuster, 1990).

7. R. Axelrod, ed., Structure of Decision: The Cognitive Maps of Political Elites (Princeton, New Jersey: Princeton University Press, 1976); and

J. Diffenbach, “Influence Diagrams for Complex Strategic Issues,” Strategic Management Journal 3 (1982): 133–146.

8. See C.W. Kirkwood and S.M. Pollack, “Multiple Attribute Scenarios, Bounded Probabilities, and Threats of Nuclear Theft,” Futures, February 1982, pp. 545–553; and

Schoemaker (1991).

9. For industry analysis, see:

M.E. Porter, Competitive Strategies (New York: Free Press, 1980).

10. A.C. Hax and N.S. Majluf, The Strategy Concept and Process: A Pragmatic Approach (New York: Prentice-Hall, 1991).

11. See R. Rumelt, “How Much Does Industry Matter?” Strategic Management Journal 12 (1991): 167–185.

12. See J.S. Bain, Industrial Organization, 2nd ed. (New York: John Wiley & Sons, 1968); and

R.A. Garda, “A Strategic Approach to Market Segmentation,” McKinsey Quarterly, Autumn 1981.

13. On forces of competition, see:

M.E. Porter, “How Competitive Forces Shape Strategy,” Harvard Business Review, March–April 1979, pp. 137–145.

On value chains, see:

M.E. Porter, Competitive Advantage (New York: Free Press, 1985).

14. D. Abell, Defining the Business (New York: Prentice-Hall, 1980), pp. 87–115.

15. P.E. Green and D.S. Tull, Research for Marketing Decisions (New York: Prentice-Hall, 1978).

16. Porter (1979).

17. C.K. Prahalad and G. Hamel, “The Core Competence of the Corporation,” Harvard Business Review, May–June 1990, pp. 79–91.

18. H. Itami, Mobilizing Invisible Assets (Cambridge, Massachusetts: Harvard University Press, 1987).

19. Amit and Schoemaker (1992).

20. See I. Dierickx and K. Cool, “Asset Stock Accumulation and Sustainability of Competitive Advantage,” Management Science 35 (1989): 1504–1514; and

Ibid.

21. J.A. De Vasconcellos and D.C. Hambrick, “Key Success Factors: Test of a General Theory in the Mature Industrial-Product Sector,” Strategic Management Journal l0 (1989): 367–382.

22. K. Ohmae, The Mind of the Strategist (New York: McGraw-Hill, 1982). Additional examples of KSFs are offered in:

De Vasconcellos and Hambrick (1989);

R.A. Irvin and E.G. Michaels, “Core Skills: Doing the Right Things Right,” The McKinsey Quarterly, Summer 1989, pp. 4–19; and Prahalad and Hamel (1990).

23. Porter (1980); and Porter (1985).

24. F.W. Gluck, “Vision and Leadership in Corporate Strategy,” in Readings on Strategic Management, ed. A. Hax (Cambridge, Massachusetts: Ballinger Publishing Co., 1984).

25. B. Tregoe and J. Zimmerman, Top Management Strategy (New York: Simon & Schuster, 1980).

26. R. Mason and I. Mitroff, Challenging Strategic Planning Assumptions (New York: John Wiley & Sons, 1981).

27. S.C. Myers, “Finance Theory and Financial Strategy,” Interfaces 14 (1984): pp. 126–137.

28. G.R. Mitchell and W.F. Hamilton, “Managing R&D as a Strategic Option,” Research Management, May–June 1988, pp. 15–22.

Comments (2)

akindele famurewa

kelly wheeler